Are homeowners in the U.S. undervaluing their properties? A new survey, when combined with data from CoreLogic, would seem to suggest they are.

By Peter Ricci

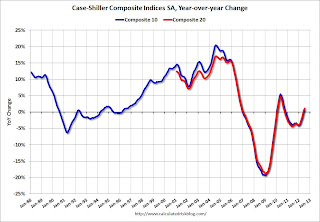

Home values have been on a certifiable roller coaster ride the last 12 years, with their ebbs and flows resembling the famed “Raging Bull” ride at Six Flags Great America; however, home values have stabilized in recent months, and have even risen in some markets – and for the first time in years, analysts are widely predicting a housing recovery.

{kind=link}

Chalk it up to home-value shell shock, but a new survey out from Rasmussen Reports suggests that homeowners may not have caught on yet with those trends, and may be undervaluing their homes against recent price gains.

Are Americans Undervaluing Their Homes?

The Rasmussen survey, which sampled 749 homeowners nationwide with these questions, found the following results:

- Forty-seven percent of homeowners say their home is worth more than what they owe on their mortgage.

- Thirty-nine percent of homeowners, though, reported that their home was worth less what they they still owe, and 14 percent were undecided.

- Generally, Rasmussen concluded that “[o]verall attitudes about the housing market remain relatively pessimistic.”

Contradictions with CoreLogic Negative Equity Data

Those poll results seem straightforward, but things get interesting when the respondents answers are compared with some of the most recent housing data, especially, as Steve Cook of Real Estate Economy Watch points out, the latest numbers on negative equity mortgages from CoreLogic – and this is where undervaluing enters the equation.

As we reported at the time, CoreLogic found that negative equity mortgages declined in the second quarter, falling from 11.4 million properties, or 23.7 percent of all mortgages, in the first quarter to 10.8 million, or 22.3 percent, in the second.

That, Cook points out, is where the data diverges. Just over 22 percent of mortgages are underwater, but 39 percent of homeowners think they are underwater? If all the data is accurate, it would indeed seem that 17 percent of homeowners are undervaluing their homes. Even more, CoreLogic reported that 1.8 million borrowers are only 5 percent underwater on their mortgages, and if recent home prices continue to increase, they too will climb out of negative equity.

So what could explain this contrast? Could some homeowners simply be worn out by negative news, and unaware of all the positive developments in housing in 2012? Give us your thoughts!