First-time homebuyers have an easier entry into the market as the year winds down because of a market sector that is having best quarter since 2000 — despite low housing inventory — largely due to historically low mortgage rates, according to a new report. The recently released First Time Homebuyer Market Report from Genworth Mortgage Insurance for the third quarter of 2017 revealed that Q3 2017 is closing out the year strong and will set the pace for a good 2018.

First-time buyers a formidable segment

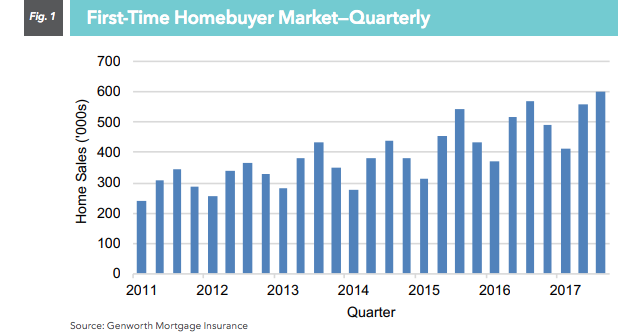

The number of sales to first-time homebuyers surpassed those to any other market segment, according to Genworth Mortgage Insurance. During Q3 first-time buyers accounted for 601,000 single-family home sales. Since 2015, the first-time homebuyer segment has made up 85 percent of the growth in single-family home sales.

“The large influx of first-time homebuyers is creating a unique challenge in the housing market,” Tian Liu, Chief Economist for Genworth wrote in a blog post. “Unlike repeat buyers, first-time homebuyers do not have a home to buy and sell at the same time.”

He continued that this is a major contributor to the lack of inventory the housing market has been experiencing lately.

Low inventory and rising prices keep the market a seller’s one

Not only is inventory for single-family homes declining as more first-time buyers are buying them up without one to put on the market, but the large number of first-time buyers has caused a spike in prices for the homes that are available.

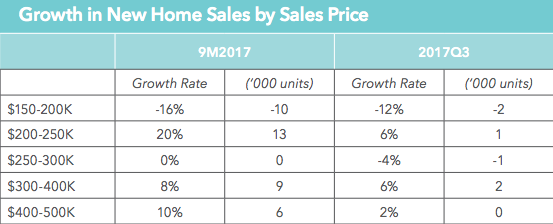

The study found that the supply of homes priced at $250,000 or less isn’t growing this year after increasing by 20 percent in 2016. The single-family inventory this quarter was concentrated on homes of $300,000 or more. This is projected to even further restrict housing sales and continue to push prices up, keeping the market a seller’s market going into 2018.

The supply of existing homes for sale during Q3 2017 stayed at an average of 4.2 months, down from last year’s 4.6 months. This has caused changes in mortgage rates and purchase loans.

Down payments are down

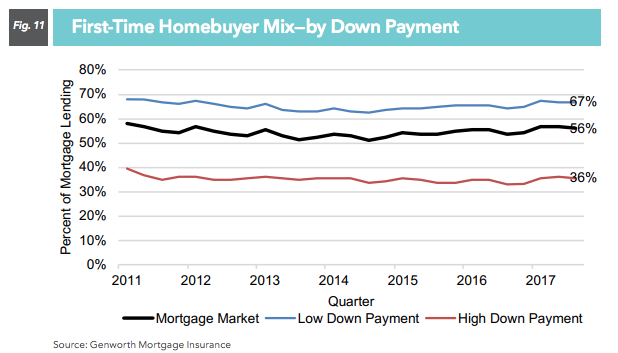

Despite increasing home prices, initial down payments are down on average for Q3 2017 (especially through private mortgage insurance companies), according to Genworth Mortgage Insurance. Low down payments, which have a loan-to-value ratio of 80 percent or higher, financed 467,000 homes for first-time buyers, which is up 5 percent since last year and accounts for 78 percent of this quarter’s first-time buyers. large down payments financed only 135,00 homes for first-time buyers. While this is only 22 percent of first-time buyers, it is up 10 percent from 2016.

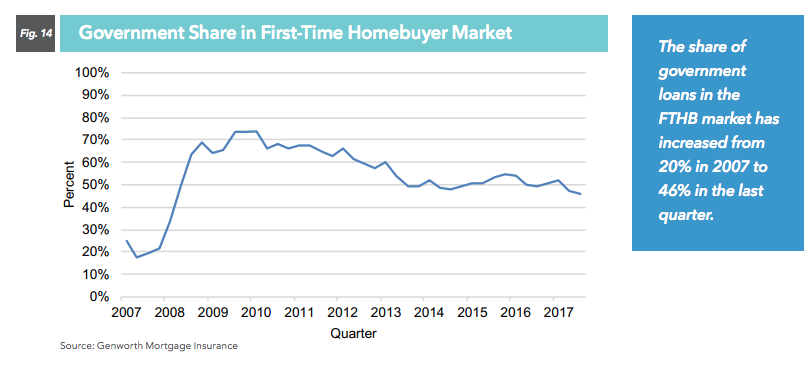

Meanwhile, government lending programs remained popular for first-time homebuyers in Q3 2017, with 46 percent of the buyers utilizing them. Government-sponsored lending programs have expanded into the purchase market in addition to the first-time buyers’ sector.